Quick links

About this series:

We’ve all seen the headlines—the economy is currently a bit of a "fixer-upper" for contractors and owners. In times like these, an executive’s real job isn't just managing the day-to-day; it’s looking over the horizon to see what’s coming before it hits the job site.

This is the second in our monthly series “Hard Hat Economics” with Dr. Anirban Basu. As the economist for the CFMA, ABC, AGC and AIA, Dr. Basu has an extraordinary ability to decode the indicators driving our industry.

Why are we doing this now? Because we believe that while you can't control the global economy, you can control how your business responds to it. Leading contractors and owners don't just wait for a turnaround—they use these moments to sharpen their tools and modernize their operations.

The economic cost of uncertainty in construction

There’s an axiom that industry loathes uncertainty. Uncertainty is not risk. Risk is fine. Risk has math. But uncertainty is an absence of guidance and data, and no construction executive wants to make external bets that are uncertain. However, the speed, amplitude and breadth of the uncertainty in the current economy draw few comparisons from history.

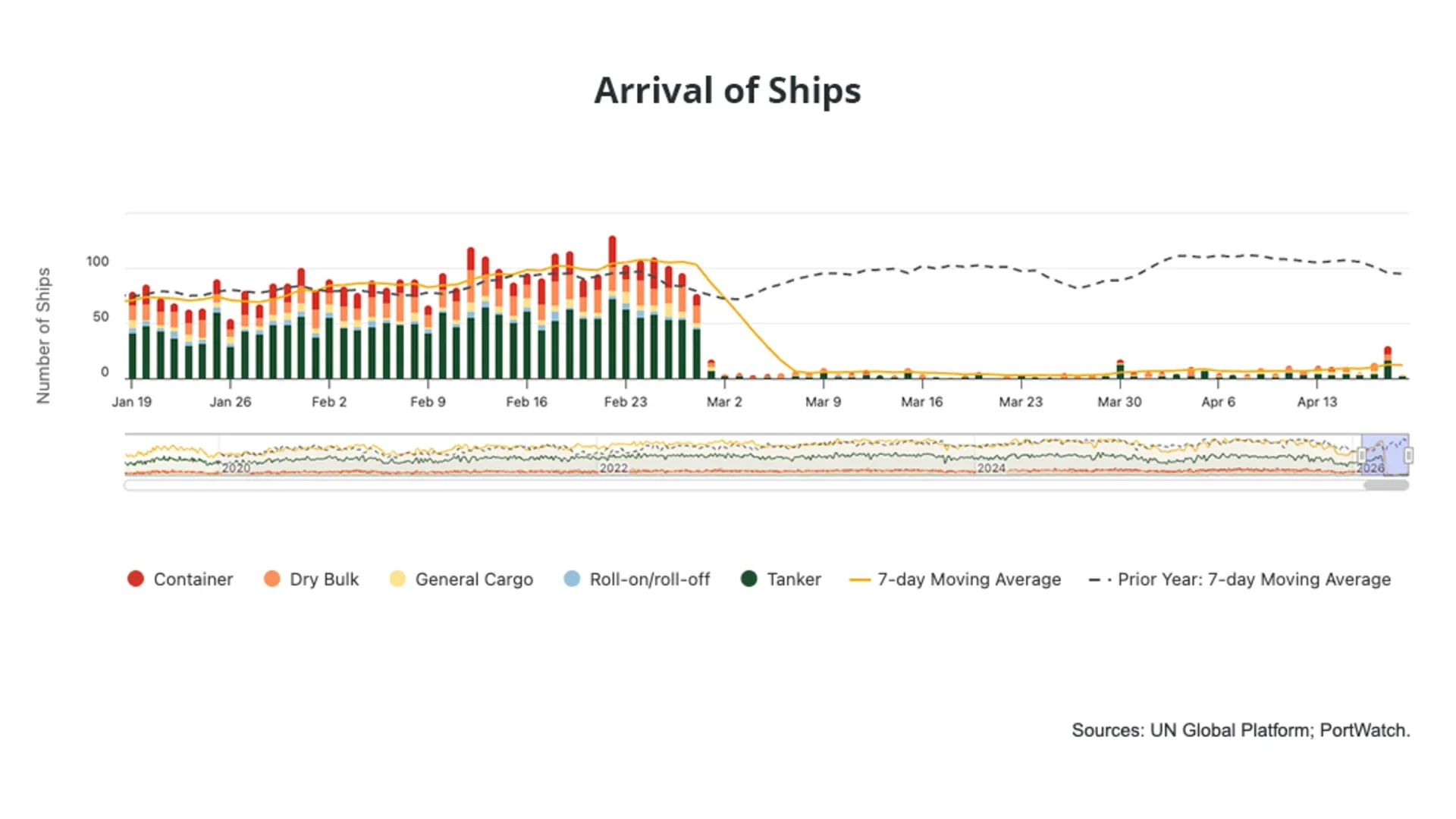

“Schrödinger’s Strait of Hormuz” casts a long shadow

Schrödinger’s cat is a popular thought experiment wherein a cat sealed in a box is both alive and dead at the same time, at least until you open the box and check. “Schrödinger’s Strait of Hormuz” is a less popular—but more relevant—thought experiment wherein one of the world’s most critical maritime chokepoints is both open and closed at the same time.

It’s open! It’s closed! It’s open and closed?

Well, at least until you open the transit data and check. Then it’s decidedly still closed, despite the fact that both the U.S. and Iran announced its reopening twice in the past two weeks, first on April 7th and then again on April 17th.

Stocks ripped, oil prices plunged and treasury yields drifted pleasantly lower following the more recently announced “reopening.” The quotation marks are entirely justified; less than 24 hours after the news broke and 12 hours after markets closed for the weekend, Iran once again declared the Strait closed.

Trust the data: it’s certainly closed.

With the exception of one incredibly brave cruise ship, transit calls through the Strait have actually declined over the past two weeks, and that’s really saying something; they were already down about 90% from pre-conflict levels.

Ship captains in the Strait of Hormuz feel the same way about uncertainty as construction executives: unwilling to risk capital (and lives) on uncertain situations. Source: IMF Port Watch

Of course, this article was written early this week when U.S. negotiators were supposed to be en route to Pakistan for meetings that may or may not be attended by their Iranian counterparts. By the time you read this, the Strait of Hormuz could be “reopened” again, or it could be reopened in a way that doesn’t necessitate quotation marks, or it could be even more closed.

It’s difficult to say what’s more worrying: that an economic update on the domestic construction industry needs a caveat that it may be stale less than 24 hours after it’s written, or that it starts with 300 words on a waterway 8,000 miles from the continental U.S.

For certain, construction input prices are up 4.8% year-over-year

The industry’s outlook would benefit greatly from a swift reopening of the Strait. Oil prices, which have fallen back from the early-April peak but are still up about $25/barrel from late-February levels, are driving up materials prices. Construction input prices surged 2.2% higher in March and were up 4.8% year over year. That’s the largest annual increase since January 2023, and April’s data will show even steeper escalation.

Labor costs up 5%, the largest increase in 2 years

This comes at a less-than-ideal time for the construction industry. Labor cost escalation has reaccelerated due to the supply-suppressing effects of immigration policy. Average hourly earnings for non-managerial construction workers were up 5.0% year over year in March, the largest annual increase in over two years. At the same time, the rise in treasury yields since the start of the conflict in Iran has pushed borrowing costs even higher.

Inflation drives borrowing costs

The Fed’s favorite measure of inflation came in hot for February, with both overall and core (excluding food and energy) prices rising 0.4% for the month. Worryingly but not surprisingly, the rate is getting faster since October last year, and further away from the Fed’s goal of 2%.

And more alarmingly, a more popular but less wonky measure of inflation came in at 0.9% for March. That’s double the rate of inflation of the worst months from the last three years. But deep breaths, everyone, that measure includes oil prices. When we exclude energy prices, inflation was up just 0.2%. And remember that oil prices have a way of sneaking their way into other costs later.

Excluding data centers, private nonresidential is down 11% since ‘23

These cost pressures will weigh on construction activity. That’s especially true for the private nonresidential segment, which has shrunk in four consecutive months and is 3% smaller than it was one year ago. Conditions would be even worse were it not for the insatiable demand for data centers; all other private nonresidential categories are down a combined 11% since the end of 2023.

One bright spot is in residential remodels, where about $1 in every $4 spent on private construction went to residential renovations in January. That’s the highest ratio since 2011. Farming revenue with small contracts and maintenance contracts explains why private equity keeps looking to invest in MEP contractors with healthy service businesses.

Uncertainty, like fear, is the mind-killer

The NFIB Small Business Optimism Index fell in March and is at its lowest level since April 2025. That’s due to higher oil prices, which “spooked consumers and owners alike.” The popular University of Michigan Consumer Sentiment Index was the lowest level ever recorded in an April. But a little caveat: those interviews were conducted before the ceasefire.

Looking ahead, it’s difficult for economists and construction executives to see through the fog of war, but a reopened Strait of Hormuz would improve the outlook for both the construction industry and broader domestic economy. In the meantime, contractors will continue to face the same issue that defined 2025: extraordinarily elevated uncertainty.

Disclaimer:

The views and opinions expressed in this article are those of Dr. Anirban Basu and do not necessarily reflect the official policy or position of Trimble Inc. This content is provided for informational purposes only and should not be interpreted as financial, investment or economic guidance from Trimble.

Recording of last month’s economics webinar—how right was Dr. Basu in his predictions?